There may never have been a federal case in history that parallels the government misconduct uncovered in the I2G case. The entire trial was based on fabricated losses and victims, as well as demonstrably false statistics. These statistics included two years’ worth of data from a completely different company that only operated after I2G had already closed.

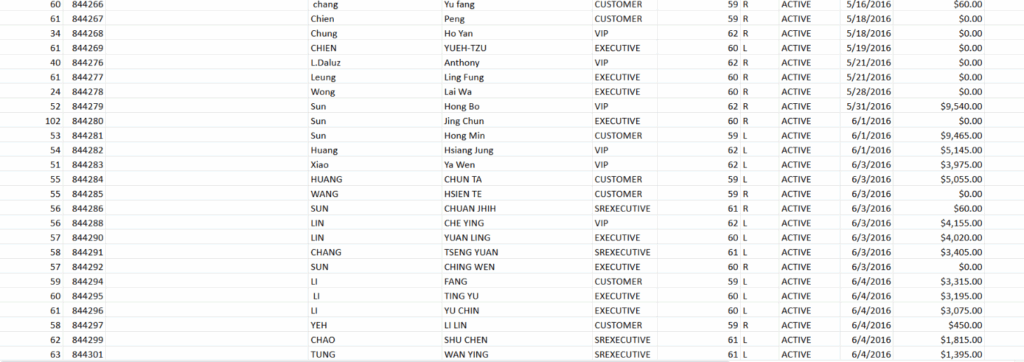

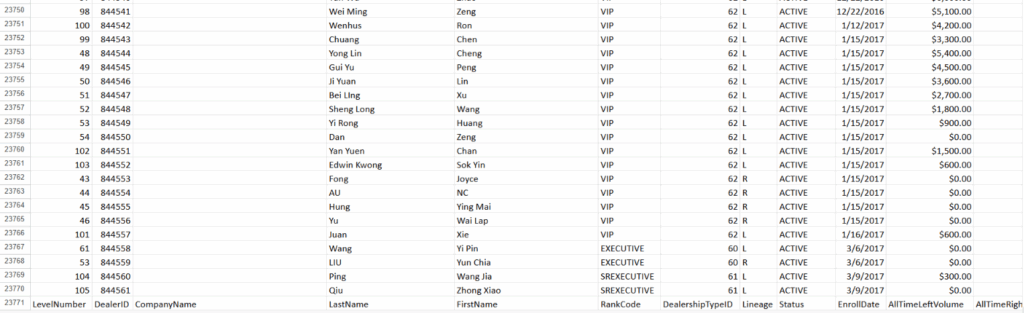

This assertion is not open to debate; it is fully verifiable through their own 7240 data, which was confirmed by their witness, who provided that information. Additionally, the seven spreadsheets, which served as key evidence for the government, included data from two years after the closure of I2G. Key Government Exhibit 101i mirrors the data found in Exhibit 101G2 below. Exhibit 101G2 reflects enrollment dates up to March 9, 2017. Notably, 4,091 enrollments occurred after the end of the I2G indictment timeline, which concluded on December 31, 2014.

The company in the data is a separate entity launched by Maike in 2015, called XTG1, based in Hong Kong. XTG1 was wholly unrelated to I2G. These critical misrepresentations in the data render invalid every claim and conclusion drawn from it, thereby invalidating all government claims. The flawed data undermines the sales figures, actual products sold, levels, commissions, gains, and losses, making all these figures unreliable.

The misleading statistics from another company, combined with over $28 million in commission data that was intentionally “filtered out” to construct Exhibit 101i, invalidated every statistical claim made by the prosecution during the trial. Not a single sales figure, distributor count, level, commission, gain, or loss was accurate.

Reynolds affirmed the reliability of the 7240 data, effectively correcting Madison Sewell’s repeated false statements in court that he had reported “problems” with the exculpatory data subpoenaed seven years before the trial. Reynolds signed an affidavit confirming that the prosecution “filtered out” key commission data equivalent to 80% of the total commissions paid out.

A review of all seven key spreadsheets used by the government shows that they extend until March 2017. This is despite testimony from government witnesses, evidence presented, and the indictment itself, which states that I2G ceased operations by December 2014 or January 2015. Jerry Reynold testified that I2G had stopped operating by the time of the FBI raid in January 2015. He falsely claimed that he had ceased working with Maike by that time, despite emails that contradict this assertion and demonstrate his knowledge of XTG1.

Throughout the trial, the government presented misleading spreadsheets that included two years of XTG1 data, which William Keep used to base his analysis of the pyramid scheme! Dr. Keep and the FTC emphasized that determining whether a company is a pyramid scheme critically relies on access to accurate company data; however, Keep’s conclusions were derived from data associated with an entirely separate company, not I2G.

The contamination of the i2g database by Xtg1 data is astonishing and should lead to the verdict being overturned. Dr. Keep emphasized that a careful study of a company’s data over time is vital to determining whether a company is operating as an illegal pyramid scheme. Dr. Keep specifically calculated a 97% loss rate, using data that filtered out $ 28 -$ 32 million in commission gains by the distributors represented in his losses!

The prosecution claims these discoveries were made too late. However, how is the truth insignificant when the prosecution deliberately concealed it to fabricate false data, losses, and victims?

The significance of Prosecutor Madison Sewell’s deliberate attempts to discredit the accurate commission data in the 7240 “All Commission Data” is that it directly contradicts every statistical claim made regarding I2G, including representations of losses and assertions regarding “victim investors.” The inflated losses and Xtg1 data undermine the entire case as well as the testimonies of 14 witnesses. This behavior should be viewed as a fraud on the court.

There is no denying that the false data representations were a fraud on the Court!

Exhibit 7240 details over 52,000 specific I2G transactions, showing $38 million in commission payments or “gains,” received by I2G distributors, or the “alleged victims,” according to the government. This information is significant because the government reported a 97% loss rate, indicating that only $7.5 million in commission gains were realized by i2G distributors. They purposefully excluded between $28 million and $32 million in commission gains from their calculations!

How can the government declare someone a “victim” without first assessing their actual commission gains? How can they determine that over $28 million in commission gains should be “filtered out” from the I2G total gains? Is it possible to find an honest answer to these questions? It seems illogical to think this was done for any reason other than to conceal the truth from the court and the jury.

How can the government claim a 97% loss rate that they know is false?

How can they assert $38 million in losses when the 7240 data shows that every single loss declaration is invalid and that the $38 million represents the “gains”?

The I2G transaction data demonstrates that the key “purchasers,” or alleged “victim investors,” upon which the indictment was based, were not victims at all. Instead, they were active and successful promoters who collected $870,000 in commissions, including direct transfers from other distributors whom they collected money from!.

Sheon Jeong, Queyenne Pepito, and Michelle Kim were presented as “victim investors” who lost hundreds of thousands of dollars. These claims, based on hearsay from McClelland and the government’s jury instructions, were damaging to the defense, which had no means to address the inaccuracies that the actual data proved. These key alleged “victim investors” did not testify, and so there was no means to challenge these claims. Sheon Jeong was depicted (through hearsay) as someone who lost over $100,000; however, the data shows that she earned over $570,000. Her commission gains are verifiable through 7240, which details 240 specific transactions, including significant direct monetary transfers amounting to tens of thousands of dollars from i2G distributors, who the data shows were also collecting money from others. Furthermore, her commission gains were utilized to purchase her products, with no attempt made by the government to deduct these commissions from her gross purchase amount or the losses presented to the jury.

Hussain was presented to the jury as a key “victim investor” whose purchase had a significant impact on a critical statute of limitations issue. However, despite this designation, Hussain was not, in fact, a “victim investor.” Government data in document 7240 shows that Hussain withdrew over $18,000, resulting in a net gain. Since Hussain did not testify, the defense had no way to refute this significant misrepresentation and the jury was asked to simply believe the prosecution’s designation.

There is no acceptable scenario in which a jury should be presented with a list labeling non-testifying individuals as “victim investors” when they are, in fact, not “victim investors.” This constitutes a fraud on the jury! The jury instructions included fraudulent loss representations by mischaracterizing distributors as “victim investors,” implying that their gross purchases were losses from “securities,” which they were not. These false representations significantly contributed to wrongful convictions. A jury cannot reach a fair verdict based on false evidence.

The jury in the i2G case was misled by inaccurate loss evidence presented through fourteen witnesses, seven spreadsheets, and two summary charts. The prosecutors cannot reasonably argue that this misinformation did not influence the jury’s decision. Every representation of loss, every product representation of Xtg1, and all summary charts and spreadsheets were invalid. Furthermore, the government failed to account for over $28 million in gains!

You can’t prove a pyramid scheme fraud with completely fake losses!

The critical evidence in document 7240 was concealed from the jury and the defense due to Prosecutor Madison Sewell’s false claims that the data provider had stated the data was inaccurate and problematic. Why did everyone trust him? The court and the defense placed their faith in Madison Sewell, believing he would act honorably and not fabricate or deliberately distort truthful information. Who plans for the government to filter out $28 million in commission gains from Reynold’s data? There was no way for the defense to predict this type of misconduct. As a result, the defendants have suffered the dire consequences.

The Constitution precludes a prosecutor from winning by trickery and deceit, then claiming the defendants didn’t discover the trickery soon enough.

While any form of misconduct by an attorney is highly problematic, misconduct by federal prosecutors is particularly egregious. As explained by the United States Supreme Court in 1935:

“The United States Attorney is the representative not of an ordinary party to a controversy but of a sovereignty whose obligation to govern impartially is as compelling as its obligation to govern at all and whose interest, therefore, in a criminal prosecution is not that it shall win a case, but that justice shall be done. As such, in a peculiar and very definite sense, he is the servant of the law, the two-fold aim of which is that guilt shall not escape or innocence suffer. He may prosecute with earnestness and vigor — indeed, he should do so. But, while he may strike hard blows, he cannot strike foul ones. It is as much his duty to refrain from improper methods calculated to produce a wrongful conviction as to use every legitimate means to bring about a just one.”

There were several instances of prosecutorial misconduct that impacted the progression of this case. The complaints about I2G did not arise organically; instead, they were the result of an extensive disinformation campaign and direct solicitations orchestrated by Chuck King, who had a specific agenda against the company. Furthermore, the government and the FBI collaborated with King, sending out over 60 solicitations to inform I2G’s distributor base that they were victims of fraud.

Shortly after FBI Agent McClelland began working with King and received several form letters which King circulated to I2G distributors, he mailed out a biased and leading survey from an address he created. This address contained the name “I2G Fraud and FBI,” which strongly implied that fraud had occurred. Despite asserting that no charges had been filed, McClelland had already claimed in a court filing that I2G was operating as a suspected criminal enterprise to secure a lis pendens.

For seven years before the trial, the “Victim Notifications” persisted without relent. Each solicitation encouraged I2G distributors and witnesses to sign up for additional victim notifications and to report suspected fraud. Since these individuals were potential witnesses for the defense and the defendants had not been convicted of any crimes, this constituted 60 counts of witness tampering in a highly egregious manner. Ultimately, only nine government distributor witnesses testified, and all of them were directly linked to either Chuck King or government solicitations.

Additionally, there were violations concerning Brady, Jenks, and Giglio that the defense did not raise. Madison Sewell received copies of Richard and Susan Anzalone’s computer, which contained both exculpatory evidence for the defendants and materials that could have been used to challenge Anzalone’s credibility at trial and question his motives for entering a plea deal. Specifically, Anzalone was directly involved in a significant Ponzi scheme called the Bit Club Network, along with his friend Joseph Abel, who was indicted and pleaded guilty in that case. This involvement provided a substantial motive for Anzalone to avoid potential indictments and to cooperate with prosecutors. Furthermore, there were two other suspected Ponzi schemes in which Anzalone was involved, which presented additional strong motives that the defense could have utilized at trial. However, the emails related to these Ponzi scheme involvements were never disclosed to the defense.

Additionally, Anzalone’s direct involvement with Xtg1, the company that Maike started after I2G, but with no involvement from Hosseinipour, undermined the narrative of an ongoing conspiracy with Hosseinipour. This also challenged all the spreadsheets used by the government throughout the trial to represent I2G up until March 2017. Furthermore, it highlighted the ongoing relationship between Maike and Anzalone, which persisted for five years after the initial indictment and just before the trial. This relationship demonstrated the trust and confidence that Anzalone had in Maike, which continued until just one month before the trial.

The defense was entitled to all these critical emails that directly impacted the credibility of their key witness against the defendants.

Previous blog articles outlined additional instances of prosecutorial misconduct, including misrepresentations of the law, presenting personal opinions as evidence, relying on hearsay as if it were factual, introducing facts not in evidence, utilizing 404(b) evidence in violation of court orders, and using the term “investment” throughout the trial despite court prohibitions.

The screenshot of the 101G 2 is available for viewing below in images 1 and 2. The government spreadsheet used at trial extended until March 2017, which was more than two years after I2G was closed. 101i was a mirror of the enrollments of 101G2 which exceeded the i2G indictment timeline by two years.

The government misrepresented twelve Xtg1 packages as I2G packages in US 101B, which included the VIP, Executive, and Senior Executive Travel Sales Software Packages. However, the government knew that I2G never offered those products. This was significant testimony used to represent total i2G sales numbers. The XTG1 packages added six million dollars in sales to the i2G total sales representations. The government presented twelve XTG1 packages along with sales numbers, incorrectly attributing those figures to I2G.

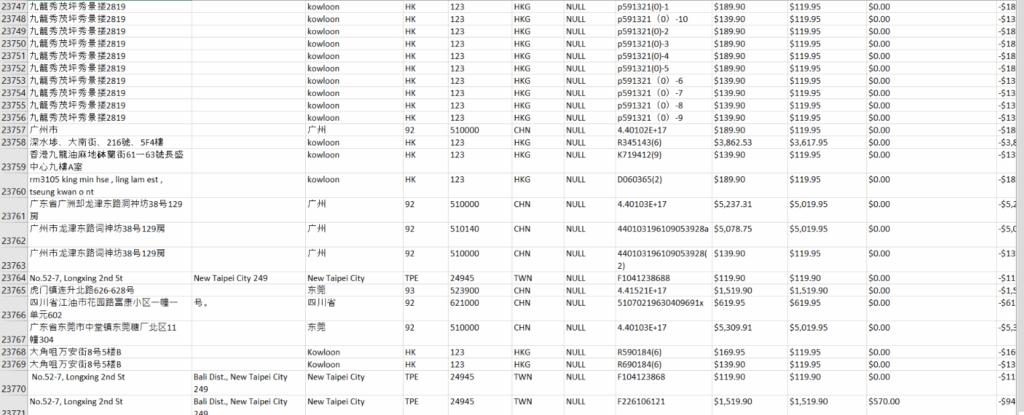

The government exhibit 101G2 contains details about 23,767 distributor entries, including 4,091 distributors who signed up between December 31, 2014, and March 9, 2017. These figures are consistent with the data presented in image 3 of document 101i. The data from 101i matches that of 101G2 and continues until March 2017, more than two years after I2G was closed.

The critical i2G data presented to the jury on seven spreadsheets included two years of XTG1 data, which did not belong to I2G at all.

The share link to 101 G 2 can be viewed here. Please note that the entry dated December 31, 2014, is numbered 19680. This marks the end of the government’s i2G timeline. The following 4,091 entries cover the period from January 1, 2014, to March 9, 2017, which is more than two years after the closure of i2G and the launch of xtg1. Additionally, these entries correspond with 101i, which also contains 4,091 entries dated after December 31, 2014.

The jury could not determine whether I2G was an alleged pyramid scheme using another company’s data – period!

The government presented the jury with over 12 product packages, valued at more than $6 million in sales, that it incorrectly attributed to I2G. In reality, these packages belonged to the Hong Kong-based company Xtg1!. The packages included items such as 101B, 12G 10054, and 12G 2–54. This was significant because Jerry Reynolds was questioned about these packages and their sales amounts. The government misrepresented these product packages as illegal recruitment packages, inflating the total sales figure by an additional $6 million, which could be described as ill-gotten gains. This constituted false evidence and was highly prejudicial in this context.

The government was aware that these were not I2G products, yet they presented them as I2G’s top product packages, despite the sales being made to Asian distributors through a completely separate company. These packages included:

VIP Monthly Subscription: $64,925.00 in sales.

VIP Travel Platform Software System: $4,222,364.00 in sales.

Executive Travel Platform and Software System: $1,130,125.25 in sales.

Senior Executive Travel Platform System: $320,905.50 in sales.

VIP Launch Promotion Pack: $39,778.05 in sales.

Executive Touch Monthly Subscriptions: $586,110.00 in sales.

Senior Executive Subscriptions: $418,125.00 in sales.

Executive to Senior Executive Upgrades: $105,595.00 in sales.

VIP Promotion Pack: $103,030.05 in sales

VIP Monthly Subscriptions $64,925.00 in sales

Senior Executive to VIP Upgrade $17,810.50

You can download 101 B below, which shows the product sales summary and the product details, proving that sales continued until March 9, 2017, two years after i2g was closed.

The data for 101G2, which reflects the enrollments for 101i, is available for download below. Please review the enrollment dates in chronological order, from earliest to latest. You will find 4,091 entries recorded between December 31, 2014, which marks the end of the i2G indictment timeline, and March 9, 2017, during the operational period of Xtg1. It is important to note that these enrollments are from Asian countries during this timeframe and are unrelated to I2G.

Notice how the final entries are all from Asia countries, including Hong Kong, where Xtg1 was based.